Why do we need Reserve Bank of India at all?If anything is to be privatized next,please do privatize the government of India first and then the RBI.Let it be a direct corporate rule!

Palash Biswas

Email:palashbiswaskl@gmail.com

Skype:palash.biswas44

* * | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

*

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

*Why do we need Reserve Bank of India at all?Our economic management is directed from IMF,World Bank,White house and MNCs worldwide.

India is highly Americanized.

US FED is a private institution.In India, every other thing is privatised.

Why not the Reserve bank of India?

It is reduced to become a tool of market forces and it designs the monetary policies while fiscal policies remain absconding since transfer of power in 1947.

RBI is not the people`s bank as the government of India is not the government of India.

If anything is to be privatised next,please do privatise the government of India first and then the RBI.

Let it be a direct coporate rule.

We have become habitual in the Open Market Economy.Purchasing capacity is our status.

We have no privacy,no sovereignty as citizen.Believe me ,it would be no difference at all.

At least, we would get rid of this power politics so disgusting!

We would get rid of all sets of scams as ingredient part and parcels of the public republic!

At least, the governance would be professional!

Nevertheless,we have to buy everything in the open market.

Those who stand out of the open market economy, they have always been subjected to ethnic cleansing!

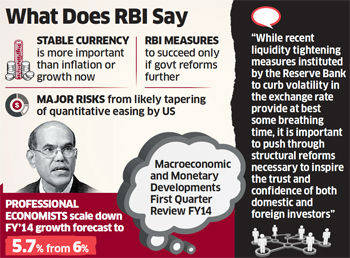

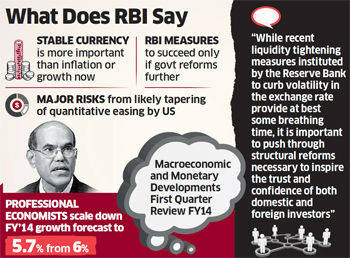

The Reserve Bank of India (RBI) in its first quarter review of monetary policy kept both the repo rate and Cash Reserve Ratio ( CRR) unchanged. This is in line with market expectations.

Maintaining an extremely hawkish stance,RBI also cut the GDP growth forecast for FY14 to 5.5% from 5.7% earlier. RBI Governor Subbarao cited various risks that are likely to hamper economic growth. Both domestic and global uncertainty were admitted to be a deterrent for economic recovery.

RBI said that it can revert to supporting growth with continuing vigil on inflation. The RBI will endeavour to keep inflation, which is under threat from a depreciating rupee, at 5 per cent by March end.

It also said that the recent liquidity tightening measures, taken to support the rupee, will be rolled back in a calibrated manner as stability is restored to the foreign exchange market, enabling it to revert to the policy of supporting growth with continuing vigil on inflation.

"The policy stance is guided by the need for continuous vigil and preparedness to pro-actively respond to risks to the economy from external developments, especially those stemming from global financial markets," Subbarao said.

The effect of the Reserve Bank's recent interest rate increase and liquidity tightening to bolster the rupee will fizzle out if the government does not move to reduce external trade imbalances, a central bank policy review says.

Giving the policy guidance, the governor said "monetary policy going forward will be shaped by the consideration of supporting growth, anchoring inflation expectations and maintaining external sector stability."

The current situation of low headline inflation, prospects of softening food inflation on a good monsoon and decelerating growth warranted a pro-growth policy stance, but for the difficulties on the external front, as reflected in the almost 10 per cent depreciation in the rupee and the rising current account deficit, he said.

Stating that the external sector was the "biggest risk to macroeconomic stability," Subbarao called for urgent policy steps from the government to curtail the CAD to a sustainable level of 2.5 per cent of GDP and said that the RBI is ready to use all instruments under its command help in the efforts.

"It should be emphasised that the time available now should be used with alacrity to institute structural measures to bring CAD down to sustainable levels," the Governor said.

The recent liquidity tightening measures, brought in to reduce speculative pressures on the rupee, which had hit a record low of 61.21 to the dollar on July 8, will be rolled back once the currency stabilises, which will lead to a shift in the monetary policy to be more accommodative and pro-growth, he added.

On inflation, while Subbarao acknowledged the ongoing rupee depreciation would create trouble for the price rise scenario, he stressed that the RBI will use all instruments at its disposal to contain it to 5 per cent by March.

Inflation as measured by wholesale prices increased marginally to 4.86 per cent in June.

Only reforms can put economy on track says Reserve Bank of India!

How does RBI spell such a verdict?

Is it replaced the Supreme court of India?

Is Indian Parliament vested in the Reserve bank of India?

Is the Government of India reincarnated in the RBI mode?

What is it?

The revival of capital inflows into India could signal the rollback of Reserve Bank of India's recent liquidity measures, C. Rangarajan, the prime minister's economic adviser, said on Tuesday.

India needs to find adequate capital inflows to finance the wide current account deficit, Rangarajan, chairman of the prime minister'sEconomic Advisory Council, told a news channel.

Reserve Bank of India left interest ratesunchanged on Tuesday as it supports a battered rupee but said it will roll back recent liquidity tightening measures when stability returns to the currency market, enabling it to resume supporting growth.

*

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

* *

*http://www.rbi.org.in/scripts/NewLinkDetails.aspx?Id=1

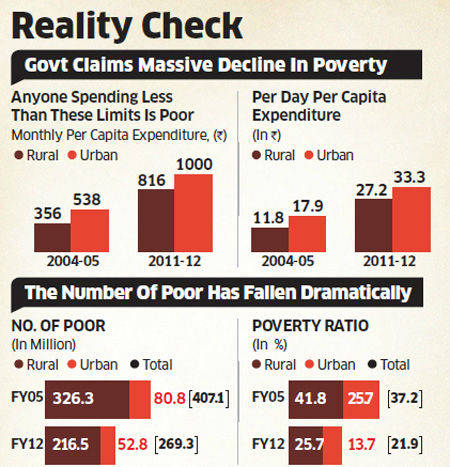

Now, only 22 per cent Indians below poverty line: Planning Commission

24 Jul, 2013

: The number of India's poor fell to less than a quarter of its population in 2011-12, according to a Planning Commission estimate, giving the government a reason to cheer amid the recent raft of disappointing macro economic data.

The commission said on Tuesday the number of those below the poverty line declined to 21.9% of the population in 2011-12, from 29.8% in 2009-10 and 37.2% in 2004-05.

The estimate, based on a survey of household consumer expenditure, showed rural poverty declined to 25.7% from 41.8% in 2004-05, while in urban areas it fell to 13.7% from 25.7%.

The sharp drop was attributed to the high real growth in recent years, which raised the consumption capacity.

The data showed that nearly 2 crore people were pulled out of poverty every year from 2004-05 onwards, which resulted in a sharp drop in those below the Tendulkar poverty line to 27 crore in 2011-12 from 40.7 crore in 2004-05.

The national level poverty ratio is based on Suresh Tendulkar methodology, which uses the mixed reference period after National Sample Survey Office (NSSO) tabulated expenditure of about 1.2 lakh households across the country.

The national poverty line has been fixed at Rs 816 per capita per month for rural areas and Rs 1,000 for urban areas.

"Thus, for a family of five, the all-India poverty line in terms of consumption expenditure would amount to about 4,080 per month in rural areas and 5,000 per month in urban areas," the Planning Commission said.

The government has set up a committee under C Rangarajan to review the Tendulkar methodology that has been criticised in the past for fixing poverty lines that were too low at 22.42 per person in rural areas and 28.65 in urban areas.

* * |

"Since the data from the NSS (National Sample Survey) 68th round (2011-12) of household consumer expenditure survey is now available, and the Rangarajan committeerecommendation will only be available a year later, the Planning Commission has updated the poverty estimates for the year 2011-12 as per the methodology recommended byTendulkar committee," the Planning Commission said in a release.

The release showed there would still be a decline in the poverty rates from 2004-05 levels even if a method other than the Tendulkar methodology was used to determine the poverty line.

Data from the survey in 2009-10 has not been used for comparison as the year was a drought year. In 2004-05, 37.2% of the country's population was below the poverty line with ratios for rural and urban areas at 41.8% and 25.7%.

The rate of decline was 0.74% per annum during the 11-year period from 1993-94 to 2004-05.

Uttar Pradesh had the highest number of poor people at 598.19 lakh, which is 29.4% of the state's total population followed by Bihar at 358.15 lakh (33.7%), Madhya Pradesh at 234.06 lakh (31.6%), Maharashtra at 197.92 lakh (17.3%) and West Bengal at 184.98 lakh (19.9%).

Prime minister Manmohan Singh had last week highlighted the UPA government's record in poverty reduction, contrasting with the lower fall in the NDA regime and earlier.

"The percentage of population below the poverty line declined at 0.75 percentage points per year before our government came to office in 2004-05. It has fallen more than 2 percentage points per year between 2004-05 and 2011-12," Singh said at an industry association function last week.

Just see the Economic Times story!

MUMBAI: The effect of the Reserve Bank's recent interest rate increase and liquidity tightening to bolster the rupee will fizzle out if the government does not move to reduce external trade imbalances, a central bank policy review says.

It will be a hard road to economic recovery as business confidence is low, and rising globalinterest rates may throw the financial markets out of gear, says the June quarter Macroeconomic and Monetary Developments review by RBI.

"While recent liquidity tightening measures instituted by the Reserve Bank to curb volatility in the exchange rate provide at best some breathing time, it is important to push through structural reforms necessary to inspire the trust and confidence of both domestic and foreign investors," says the review by the central bank's research team.

* * |

Governor DuvvuriSubbarao's interest rate action need not reflect his research team's view.

The rupee's fall to a record low of 61.20 to the US dollar on July 8 triggered a series of measures from RBI that raised short-term interest rates on bonds and commercial paper by as much as 300 basis points. A basis point is 0.01 percentage point. The currency also gained past 59 to the greenback, but has since fallen to end Monday at 59.41.

Blaming the excess liquidity in the system for speculation on the currency, RBI has capped the amount available under the liquidity adjustment facility to 0.5% of total liabilities.

Mixed picture of economy

It has raised penal interest rates under the Marginal Standing Facility by 200 basis points to 10.25%, effectively making it the repo rate for the short term.

"Right now the focus for RBI is on rupee," said Ananth Narayan, head of treasury at Standard Chartered Bank. "There is only so much that RBI can do, and it expects the government to take steps."

Delays in project clearances and policy imbroglio such as foreign direct investment in multi-brand retail have eroded business confidence. Although it has succeeded in reducing gold imports that accounted for more than half the current account deficit, the lack of exports push is reducing US dollar inflows.

"This strategy will succeed only if reinforced by structural reforms to reduce current account deficit and step up savings and investment," said RBI.

Current account deficit moderated to 3.8% of GDP in the fourth quarter from a high of 6.5% in the December quarter. Some estimate it to climb again for the June quarter.

The assessment of the economy reveals a mixed picture. While RBI's own industrial outlook survey indicates a marginal improvement in the level of business optimism, surveys by private agencies point to weak business expectations.

Professional economists have scaled down their growth forecast for the year to 5.7%, from 6%.

"Leading indicators do not suggest immediate improvement in production activity and a slow-paced recovery is likely to shape only later in 2013-14, supported by a good monsoon that could shore up rural demand," said the RBI report.

The central bank has also warned of a possible disruption in global financial markets with the Federal Reserve likely to taper off its quantitative easing by reducing $85 billion of bond purchases.

RBI can't afford to frighten equity investors

One can only hope that having done what it did over the past fortnight, RBI will now weigh its words carefully to prevent the carnage in the bond market from boiling over to stocks.

Having indirectly raised interest rates by 300 basis points and the cash reserve ratio by half a point, Governor Subbarao cannot give up his hawkish stance. But, if he's ultra hawkish, he could end up frightening the stock market that has fallen continuously since the last round of measures.

Till now, FII selling in equities has not been alarming; this is because the equity investorsstrongly believe that RBI's tightening measures are short-term and aimed at stabilising currency (not taming inflation). This belief has to be preserved at all cost, simply because if FIIs start dumping stocksno amount of tightening and pep talk can rein in the rupee.

Not that the measures have had a significant impact (with the rupee still closing well below 59). It's possible that the rupee's modest appreciation could have been achieved even without choking the money market, just as other emerging markets that have seen their currencies gain without tightening. RBI, nonetheless, may try to communicate that it's the actions that are working to stabilise the outlook on rupee.

But what if the measures stop working? Unwinding them too soon could put the rupee again under pressure. What was partly successful in '98 when RBI had adopted similar measures could be less effective today: India is far more liberalised and exposed to international markets than it was in '98, and the scope of stabilizing rupee through monetary measures is more limited today than it was then.

The macro-economic environment too was different: forex coverage of external debt is three-times as much today compared with 1997-98; growth in 2013 is slower and inflation more benign than what it was 1997-98; so are deposit and money supply growth which rule out concerns of overheating.

The off shore non-deliverable market for rupee in '97/98 was a fraction of what it is today when a flourishing offshore market, like the proverbial tail wagging the dog, often influences the exchange rate at home. And most importantly, the gap between US and Indian interest rates is much wider today than what it was 15 years ago.

Those were also the days when government could privately place bonds with RBI and keep its borrowing cost well below the market rates. Not any more; today, the market will demand a competitive rate from the government similar to what it would charge any other borrower.

The changed realities make one wonder whether the measures were warranted at all. However, the more important task at hand is finding an orderly way to unwind them and lining up new dollar inflows through FDI, and sovereign bonds or NRI deposits.

Poverty line low, need to revisit methodology, says Montek Singh Ahluwalia

NEW DELHI: Planning commission deputy chairman Montek Singh Ahluwalia on Monday admitted that the latest poverty estimates released last week is indeed low and needs to be revised upward.

The commission said last week that only 21.9% of the population was poor, based on a per capita spending of 33.33 day in cities and 27.20 rural India, causing widespread outrage for being too low.

"As the country becomes richer and the per capita income goes up, there is need to redefine the poverty line. The latest numbers that planning commission have released, based on the Tendulkar Committee report, are absolutely rock-bottom numbers and gives us the number of poor who are actually the weakest group and therefore, should be the priority of the government," Ahluwalia said.

Based on this cut off, there were 269.3 million poor in India in 2011-12 against 407.1 million in 2004-05. If the poverty cut off is revised, the number of poor could increase again.

Ahulwalia said poverty has fallen at a faster pace during UPA regime and even the absolute numbers have come down as compared to the previous government. The last poverty estimates, based on the National Sample Survey, had come in 2004-05 and 2009-10. However, government did not consider the numbers of 2009-10 saying that it was a drought year and would not convey the real picture.

* * |

Hence, NSSO conducted a survey once again, based on which planning commission released the poverty estimates for 2011-12, the last year of the 11th plan period. According to latest estimates of the Planning Commission, the poverty ratio, or population of poor in the country, dipped to 21.9% in 2011-12 from 37.2% in 2004-05 due to an increase in per capita consumption.

This was a decline of 2.2% per annum since 2004-05 vis-a-vis 0.74% in the tenure of previous government, the Planning Commission had said. Besides, the absolute poverty numbers also declined, pulling out nearly 130 million people out of poverty in seven years of UPA regime.

The plan panel had used the Suresh Tendulkar Committee's methodology, which factors in spending on health and education besides calorie intake to arrive at a poverty line for cities and villages. Accordingly, those whose daily consumption of goods and services exceed 33.33 in cities and 27.20 in villages are not poor.

This has drawn lot of criticism from the opposition and from within the party. Since there has been similar criticism in the past, government has already set up a committee under Prime Minister's Economic Advisory Council chairman C Rangarajan to revisit the methodology for tabulating poverty.

The committee is expected to submit its report by middle of next year and Ahulwalia says he is confident of seeing an increase in absolute poverty numbers when the Rangarajan committee's recommendations are out.

Planning Commission sticks to old formula to define poor

By Mahendra Singh, TNN | 24 Jul, 2013, 10.51AM IST

NEW DELHI: People spending more than Rs 27.2 per day in villages and Rs 33.3 in cities are not poor, according to latest data released by the government.

The proportion of the poor has come down to 21.9% of the country's population in 2011-12 from 37.2% in 2004-05, a decline of 2.18 percentage points every year during seven years of UPA rule.

The absolute number of poor declined by nearly 137.4 million between 2004-05 and 2011-12 and by around 85 million between 2009-10 and 2011-12.

However, there are still 269.7 million poor — 217.2 million in villages and 53.1 million in cities — across the country as against 407.3 million in 2004-05.

The percentage of persons below the poverty line in 2011-12 has been estimated at 25.7% in rural areas and 13.7% in urban areas.

The sharp decline in poverty levels across the country is based on the benchmark of a fresh poverty line. But the timing and the methodology for estimating poverty is questionable as the fresh estimates are based on the Tendulkar methodology, which was junked by the Planning Commission last year after a huge public outcry.

The plan panel's earlier figures showed that poverty was declining by 1.5 percentage points from 37.2% to 29.8% between 2004-05 and 2009-10, but the data was disowned after it was criticized for pegging the poverty line too low at Rs 22.42 per person per day in rural areas and Rs 28.65 in urban areas.

After intervention from the UPA's top leadership, the government set up another committee headed by C Rangarajan to look at a methodology for determining poverty lines and estimating poverty.

The commission justified the release of the data using the old methodology saying the data from the National Sample Survey (NSS) 68th round (2011-12) was now available and theRangarajan committee recommendation will only be available in mid-2014 so it had updated the poverty estimates for the year 2011-12 as per the methodology recommended by theTendulkar committee.

After the controversy, a special survey was conducted by the NSSO to determine poverty, an exercise which taken up after a gap of five years.

The official argument is that whatever be the poverty line, there will be a decline in poverty in percentage terms.

The commission argued that it is important to note that although the declining trend is based on the Tendulkar poverty line, which is being reviewed and may be revised by the Rangarajan committee, an increase in the poverty line will not alter the fact of a decline. "While the absolute levels of poverty would be higher, the rate of decline would be similar," it said.

Reserve Bank of India

From Wikipedia, the free encyclopedia

| Reserve Bank of India भारतीय रिज़र्व बैंक | |||||

| | ||||

| Headquarters | |||||

Established | 1 April 1935 | ||||

Currency | Indian rupee (₹) | ||||

ISO 4217 Code | INR | ||||

Reserves | |||||

Base borrowing rate | 7.50% | ||||

Base deposit rate | 6.00% | ||||

Website |

*

* *

*The Reserve Bank of India (RBI) is India's central banking institution, which formulates the monetary policy with regard to the Indian rupee. It was established on 1 April 1935 during the British Raj in accordance with the provisions of the Reserve Bank of India Act, 1934.[2] The share capital was divided into shares of ₹100 each fully paid, which was entirely owned by private shareholders in the beginning.[3] Following India's independence in 1947, the RBI was nationalised in the year 1949.

Contents

[hide]

Purposes and structure[edit]

RBI assumes an important part in the development strategy of the Government of India, and as a leading member of the Alliance for Financial Inclusion (AFI), a global network of financial policymakers from developing and emerging countries working together to increase access to appropriate financial services for the poor. RBI is also a member of the Asian Clearing Union. The general superintendence and direction of the RBI is entrusted with the 21-member-strong Central Board of Directors—the Governor (currentlyDuvvuri Subbarao), four Deputy Governors, two Finance Ministry representatives, ten government-nominated directors to represent important elements from India's economy, and four directors to represent local boards headquartered at Mumbai, Kolkata, Chennai and New Delhi. Each of these local boards consists of five members who represent regional interests, as well as the interests of co-operative and indigenous banks.

History[edit]

1935–1950[edit]

The old RBI Building in Mumbai

The Reserve Bank of India (RBI) was founded on 1 April 1935 to respond to economic troubles after the First World War. The bank was set up based on the recommendations of the 1926 Royal Commission on Indian Currency and Finance, also known as the Hilton Young Commission[4]. It began according to the guidelines laid down by Dr. B. R. Ambedkar, whose guidelines, working style and outlook were presented to the Hilton Young Commission. When this Commission came to India, under the name of "Royal Commission on Indian Currency and Finance", every member of this Commission was holding Dr. Ambedkar's book titled The problem of the rupee: its origin and its solution.[5] The Commission also was advised by John Maynard Keynes, a member of the Commission.[6][7]

The original choice for the seal of RBI was The East India Company Double Mohur, with the sketch of the Lion and Palm Tree. However it was decided to replace the lion with the tiger, the national animal of India. The Preamble of the RBI describes its basic functions to regulate the issue of bank notes, keep reserves to secure monetary stability in India, and generally to operate the currency and credit system in the best interests of the country.

The Central Office of the RBI was initially established in Calcutta (now Kolkata), but was permanently moved to Bombay (now Mumbai) in 1937. The RBI also acted as Burma's central bank, except during the years of the Japanese occupation of Burma (1942–45), until April 1947, even though Burma seceded from the Indian Union in 1937. After the Partition of India in 1947, the Bank served as the central bank for Pakistan until June 1948 when the State Bank of Pakistan commenced operations. Though originally set up as a shareholders' bank, the RBI has been fully owned by the Government of India since its nationalization in 1949.[8]

1950–1960[edit]

In the 1950s, the Indian government, under its first Prime Minister Jawaharlal Nehru, developed a centrally planned economic policy that focused on the agricultural sector. The administration nationalized commercial banks[9] and established, based on the Banking Companies Act of 1949 (later called the Banking Regulation Act), a central bank regulation as part of the RBI. Furthermore, the central bank was ordered to support the economic plan with loans.[10]

1960–1969[edit]

As a result of bank crashes, the RBI was requested to establish and monitor a deposit insurance system. It should restore the trust in the national bank system and was initialized on 7 December 1961. The Indian government founded funds to promote the economy and used the slogan "Developing Banking". The government of India restructured the national bank market and nationalized a lot of institutes. As a result, the RBI had to play the central part of control and support of this public banking sector.

1969–1985[edit]

In 1969, the Indira Gandhi-headed government nationalized 14 major commercial banks. Upon Gandhi's return to power in 1980, a further six banks were nationalized.[11] The regulation of the economy and especially the financial sector was reinforced by the Government of India in the 1970s and 1980s.[12] The central bank became the central player and increased its policies for a lot of tasks like interests, reserve ratio and visible deposits.[13] These measures aimed at better economic development and had a huge effect on the company policy of the institutes. The banks lent money in selected sectors, like agri-business and small trade companies.[14]

The branch was forced to establish two new offices in the country for every newly established office in a town.[15] The oil crises in 1973 resulted in increasing inflation, and the RBI restricted monetary policy to reduce the effects.[16]

1985–1991[edit]

A lot of committees analysed the Indian economy between 1985 and 1991. Their results had an effect on the RBI. The Board for Industrial and Financial Reconstruction, the Indira Gandhi Institute of Development Research and the Security & Exchange Board of India investigated the national economy as a whole, and the security and exchange board proposed better methods for more effective markets and the protection of investor interests. The Indian financial market was a leading example for so-called "financial repression" (Mackinnon and Shaw).[17] The Discount and Finance House of India began its operations on the monetary market in April 1988; theNational Housing Bank, founded in July 1988, was forced to invest in the property market and a new financial law improved the versatility of direct deposit by more security measures and liberalisation.[18]

1991–2000[edit]

The national economy came down in July 1991 and the Indian rupee was devalued.[19] The currency lost 18% relative to the US dollar, and the Narsimahmam Committee advised restructuring the financial sector by a temporal reduced reserve ratio as well as the statutory liquidity ratio. New guidelines were published in 1993 to establish a private banking sector. This turning point should reinforce the market and was often called neo-liberal.[20] The central bank deregulated bank interests and some sectors of the financial market like the trust and property markets.[21] This first phase was a success and the central government forced a diversity liberalisation to diversify owner structures in 1998.[22]

The National Stock Exchange of India took the trade on in June 1994 and the RBI allowed nationalized banks in July to interact with the capital market to reinforce their capital base. The central bank founded a subsidiary company—the Bharatiya Reserve Bank Note Mudran Limited—in February 1995 to produce banknotes.[23]

Since 2000[edit]

The Foreign Exchange Management Act from 1999 came into force in June 2000. It should improve the foreign exchange market, international investments in India and transactions. The RBI promoted the development of the financial market in the last years, allowedonline banking in 2001 and established a new payment system in 2004–2005 (National Electronic Fund Transfer).[24] The Security Printing & Minting Corporation of India Ltd., a merger of nine institutions, was founded in 2006 and produces banknotes and coins.[25]

The national economy's growth rate came down to 5.8% in the last quarter of 2008–2009[26] and the central bank promotes the economic development.[27]

Structure[edit]

RBI runs a monetary museum in Mumbai

Central Board of Directors[edit]

The Central Board of Directors is the main committee of the central bank. The Government of India appoints the directors for a four-year term. The Board consists of a governor, four deputy governors, fifteen directors to represent the regional boards, one from the Ministry of Finance and ten other directors from various fields. The Government nominated Arvind Mayaram, as a director of the Central Board of Directors with effect from August 7, 2012 and vice R Gopalan, RBI said in a statement on August 8, 2012. .[28] The Central Government has nominated Shri Rajiv Takru, Secretary, Department of Financial Services, Ministry of Finance, New Delhi as a director on the Central Board of Directors of the Reserve Bank of India vice Shri D. K. Mittal. Shri Takru's nomination is with effect from February 4, 2013 and until further orders.[29] IJI0-0==0-990YFYU

Governors[edit]

The current Governor of RBI is Duvvuri Subbarao. The RBI extended the period of the present governor up to 2013. There are four deputy governors presently, Deputy Governor K C Chakrabarty, Urjit patel, Anand Sinha and H.R. Khan. Deputy Governor K C Chakrabarty's term has been extended further by 2 years.[30]

Supportive bodies[edit]

The Reserve Bank of India has ten regional representations: North in New Delhi, South in Chennai, East in Kolkata and West in Mumbai. The representations are formed by five members, appointed for four years by the central government and serve—beside the advice of the Central Board of Directors—as a forum for regional banks and to deal with delegated tasks from the central board.[31] The institution has 22 regional offices.

The Board of Financial Supervision (BFS), formed in November 1994, serves as a CCBD committee to control the financial institutions. It has four members, appointed for two years, and takes measures to strength the role of statutory auditors in the financial sector, external monitoring and internal controlling systems.

The Tarapore committee was set up by the Reserve Bank of India under the chairmanship of former RBI deputy governor S. S. Tarapore to "lay the road map" to capital account convertibility. The five-member committee recommended a three-year time frame for complete convertibility by 1999–2000.

On 1 July 2007, in an attempt to enhance the quality of customer service and strengthen the grievance redressal mechanism, the Reserve Bank of India created a new customer service department.

Offices and branches[edit]

The Reserve Bank of India has four zonal offices.[32] It has 19 regional offices at most state capitals and at a few major cities in India. Few of them are located in Ahmedabad, Bangalore, Bhopal, Bhubaneswar, Chandigarh, Chennai, Delhi, Guwahati, Hyderabad, Jaipur,Jammu, Kanpur, Kolkata, Lucknow, Mumbai, Nagpur, Patna, and Thiruvananthapuram. Besides it has 09 sub-offices at Agartala,Dehradun, Gangtok, Kochi, Panaji, Raipur, Ranchi, Shillong, Shimla and Srinagar.

The bank has also two training colleges for its officers, viz. Reserve Bank Staff College at Chennai and College of Agricultural Banking at Pune. There are also four Zonal Training Centres at Mumbai, Chennai, Kolkata and New Delhi.

Main functions[edit]

Reserve Bank of India regional office, Delhi entrance with the Yakshini sculpture depicting "Prosperity through agriculture".[33]

The RBI Regional Office in Delhi.

The regional office of RBI (in sandstone)in front of GPO(in white) at Dalhousie Square,Kolkata.

Bank of Issue[edit]

Under Section 22 of the Reserve Bank of India Act, the Bank has the sole right to issue bank notes of all denominations. The distribution of one rupee notes and coins and small coins all over the country is undertaken by the Reserve Bank as agent of the government. The Reserve Bank has a separate Issue Department which is entrusted with the issue of currency notes. The assets and liabilities of the Issue Department are kept separate from those of the Banking Department.

Monetary authority[edit]

The Reserve Bank of India is the main monetary authority of the country and beside that, in its capacity as the central bank, acts as the bank of the national and state governments. It formulates, implements and monitors the monetary policy as well as it has to ensure an adequate flow of credit to productive sectors.

Regulator and supervisor of the financial system[edit]

The institution is also the regulator and supervisor of the financial system and prescribes broad parameters of banking operations within which the country's banking and financial system functions.Its objectives are to maintain public confidence in the system, protect depositors' interest and provide cost-effective banking services to the public. The Banking Ombudsman Scheme has been formulated by the Reserve Bank of India (RBI) for effective addressing of complaints by bank customers. The RBI controls the monetary supply, monitors economic indicators like the gross domestic product and has to decide the design of the rupee banknotes as well as coins.[34]

Management of foreign exchange[edit]

The RBI is in charge of facilitating the achievement of the goals of the Foreign Exchange Management Act, 1999. Objective: to facilitate external trade and payment and promote orderly development and maintenance of foreign exchange market in India.

Issuer of currency[edit]

The bank issues and exchanges or destroys currency notes and coins that are not fit for circulation. The objectives are to give the public an adequate supply of currency of good quality and to provide loans to commercial banks to maintain or improve the GDP. The basic objectives of RBI are to issue bank notes, to maintain the currency and credit system of the country, and to maintain the reserves. RBI maintains the economic structure of the country so that it can achieve the objectives of price stability as well as economic development, because both objectives are diverse in themselves

* * | This article may be confusing or unclear to readers.Please help us clarify the article; suggestions may be found on the talk page. (July 2013) |

.

Banker of banks[edit]

Nagpur branch holds most of India's gold deposits

RBI also works as a central bank where commercial banks are account holders and can deposit money. RBI maintains banking accounts of all scheduled banks.[35]Commercial banks create credit. It is the duty of the RBI to control the credit through the CRR, bank rate and open market operations. As the bankers' bank, the RBI facilitates the clearing of cheques between the commercial banks and helps inter-bank transfer of funds. It can grant financial accommodation to schedule banks. It acts as the lender of last resort by providing emergency advances to the banks. It supervises the functioning of the commercial banks and take action against it if need arises.

Detection of fake currency[edit]

In order to curb the fake currency menace, RBI has launched a website to raise awareness among masses about fake notes in the market.www.paisaboltahai.rbi.org.in provides information about identifying fake currency.[36]

Developmental role[edit]

The central bank has to perform a wide range of promotional functions to support national objectives and industries.[10] The RBI faces a lot of inter-sectoral and local inflation-related problems. Some of this problems are results of the dominant part of the public sector.[37]

Related functions[edit]

The RBI is also a banker to the government and performs merchant banking function for the central and the state governments. It also acts as their banker. The National Housing Bank (NHB) was established in 1988 to promote private real estate acquisition.[38] The institution maintains banking accounts of all scheduled banks, too. RBI on 7 August 2012 said that Indian banking system is resilient enough to face the stress caused by the drought like situation because of poor monsoon this year.[39]

Policy rates and reserve ratios[edit]

| Bank Rate | 10.25%(16/7/2013) |

Repo Rate | 7.25% |

Reverse Repo Rate | 6.25% |

Cash Reserve Ratio (CRR) | 4% |

Statutory Liquidity Ratio (SLR) | 23.0% |

Base Rate | 9.75%–10.50% |

Reserve Bank Rate | 4% |

Deposit Rate | 8.50%–9.0% |

Bank Rate[edit]

RBI lends to the commercial banks through its discount window to help the banks meet depositor's demands and reserve requirements for long term. The Interest rate the RBI charges the banks for this purpose is called bank rate. If the RBI wants to increase the liquidity and money supply in the market, it will decrease the bank rate and if RBI wants to reduce the liquidity and money supply in the system, it will increase the bank rate. As of 16 July 2013, the bank rate was 10.25%.

Reserve requirement cash reserve ratio (CRR)[edit]

Every commercial bank has to keep certain minimum cash reserves with RBI. Consequent upon amendment to sub-Section 42(1), the Reserve Bank, having regard to the needs of securing the monetary stability in the country, RBI can prescribe Cash Reserve Ratio (CRR) for scheduled banks without any floor rate or ceiling rate, [Before the enactment of this amendment, in terms of Section 42(1) of the RBI Act, the Reserve Bank could prescribe CRR for scheduled banks between 5% and 20% of total of their demand and time liabilities]. RBI uses this tool to increase or decrease the reserve requirement depending on whether it wants to effect a decrease or an increase in the money supply. An increase in Cash Reserve Ratio (CRR) will make it mandatory on the part of the banks to hold a large proportion of their deposits in the form of deposits with the RBI. This will reduce the size of their deposits and they will lend less. This will in turn decrease the money supply. Due to a Reduction in CRR by 0.25% (25 basis points cut in Cash Reserve Ratio(CRR)) on 17 September 2012, Rs 17,000 crore was released into the system/market. The RBI lowered the CRR by 25 basis points to 4.25% on 30 October 2012, a move it said would inject about 175 billion rupees into the banking system in order to pre-empt potentially tightening liquidity. The latest CRR is 4% (wef 09/02/2013).

Statutory Liquidity ratio (SLR)[edit]

Apart from the CRR, banks are required to maintain liquid assets in the form of gold, cash and approved securities. Higher liquidity ratio forces commercial banks to maintain a larger proportion of their resources in liquid form and thus reduces their capacity to grant loans and advances, thus it is an anti-inflationary impact. A higher liquidity ratio diverts the bank funds from loans and advances to investment in government and approved securities.

In well-developed economies, central banks use open market operations—buying and selling of eligible securities by central bank in the money market—to influence the volume of cash reserves with commercial banks and thus influence the volume of loans and advances they can make to the commercial and industrial sectors. In the open money market, government securities are traded at market related rates of interest. The RBI is resorting more to open market operations in the more recent years.

Generally RBI uses three kinds of selective credit controls:

Minimum margins for lending against specific securities.

-

Ceiling on the amounts of credit for certain purposes.

-

Discriminatory rate of interest charged on certain types of advances.

Direct credit controls in India are of three types:

Part of the interest rate structure i.e. on small savings and provident funds, are administratively set.

-

Banks are mandatory required to keep 23% of their deposits in the form of government securities.

Banks are required to lend to the priority sectors to the extent of 40% of their advances.

Further reading[edit]

S. L. N. Simha. History of the Reserve Bank of India, Volume 1: 1935–1951. RBI. 1970. ISBN 81-7596-247-X. (2005 reprint PDF)

G. Balachandran. The Reserve Bank of India, 1951–1967. Oxford University Press. 1998. ISBN 0-19-564468-9. (PDF)

A. Vasudevan et al. The Reserve Bank of India, Volume 3: 1967–1981. RBI. 2005. ISBN 81-7596-299-2. (PDF)

Cecil Kisch: Review "The Monetary Policy of the Reserve Bank of India" by K. N. Raj. In: The Economic Journal. Vol. 59, No. 235 (Sep., 1949), pp. 436–438.

Findlay G. Shirras: The Reserve Bank of India. In The Economic Journal. Vol. 44, No. 174 (Jun., 1934), pp. 258–274.

Narenda Jadhav, Partha Ray, Dhritidyuti Bose, Indranil Sen Gupta: The Reserve Bank of India's Balance Sheet: Analytics and Dynamics of Evolution, November 2004.

Notes[edit]

References[edit]

^ a b Press Trust of India (25 December 2011 16:20). "India's forex reserves slump by $4.67 billion". Mumbai: New Delhi Television Limited. Retrieved 5 January 2012.

^ "Reserve Bank of India Act, 1934". p. 115. Retrieved August 6, 2012.

^ "RESERVE BANK OF INDIA ACT, 1934 (As modified up to 27 February 2009)". Reserve Bank of India (RBI). Retrieved 20 November 2010.

^ Royal Commission on Indian Currency and Finance, H. M. Stationery Office (1926)

^ B. R. Ambedkar, The problem of the rupee: its origin and its solution. P. S. King & Son, London (1923).

^ The London Gazette: no. 28711. p. 2809. 18 April 1913. Retrieved 4 August 2009.

^ See Keynes, John Maynard (1913), Indian Currency and Finance, London: Macmillan & Co.

^ Beth Anne Wilson und Geoffrey N. Keim: India and the Global Economy in Business Economics, January 2006, S.29.

^ a b Narenda Jadhav, Partha Ray, Dhritidyuti Bose, Indranil Sen Gupta: The Reserve Bank of India's Balance Sheet: Analytics and Dynamics of Evolution, November 2004, S.. 16.

^ "Reserve Bank of India: Platinum Jubilee (PDF)". RBI.org.in. 2010. Retrieved on 15 April 2012.

^ Ananya Mukherjee Reed: Corporate Governance Reforms in India in Journal of Business Ethics, Volume 37, Number 3 / May, 2002, p. 253.

^ Sunil Kumar, Rachita Gulati: Did efficiency of Indian public sector banks converge with banking reforms? in Int Rev Econ (2009) 56:47–84, p. 47-48.

^ Panicos O. Demetriades, Kul B. Luintel: Financial Development, Economic Growth and Banking Sector Controls: Evidence from India. in The Economic Journal. Vol. 106, No. 435 (March 1996), pp. 359–374, p. 360.

^ Alpana Killawala: "History of The Reserve Bank of India – Summary", Reserve Bank of India Press Release, 18.03.2006 (RBI)

^ Narenda Jadhav, Partha Ray, Dhritidyuti Bose, Indranil Sen Gupta: The Reserve Bank of India's Balance Sheet: Analytics and Dynamics of Evolution, November 2004, S. 40.

^ Sunil Kumar, Rachita Gulati: Did efficiency of Indian public sector banks converge with banking reforms? in Int Rev Econ (2009) 56:47–84, p. 48.

^ Chronology of Events, Developing the Markets: Seeds of Liberalization- 1985 to 1991 (RBI)

^ Amal Kanti Ray: India's Social Development in a Decade of Reforms: 1990–91/1999–2000 in Social Indicators Research, Volume 87, Number 3 / July, 2008, p. 410.

^ Ananya Mukherjee Reed: Corporate Governance Reforms in India in Journal of Business Ethics, Volume 37, Number 3 / May, 2002, p. 257.

^ Raghbendra Jha, Ibotombi S. Longjam: Structure of financial savings during Indian economic reforms in Empirical Economics (2006) 31:861–869, p.862.

^ Sunil Kumar, Rachita Gulati: Did efficiency of Indian public sector banks converge with banking reforms? in Int Rev Econ (2009) 56:47–84, p. 49,

^ Chronology of Events, Crisis and Reforms- 1991 to 2000(RBI)

^ "RBI History – Spanning 7 Decades of Public Service". Rbidocs.rbi.org.in. 1935-04-01. Retrieved 2010-08-20.

^ Security Printing &Minting Corporation of India, About Us(SPMCIL)

^ Second Quarter Review of Monetary Policy for the Year 2009–10, Punkt 15., (RBI)

^ Macroeconomic and Monetary Developments – Second Quarter Review 2009–10, S.94, (RBI)

^ "Arvind Mayaram nominated as director in RBI board". 08-08-2012.

^ "Rajiv Takru nominated as a director on the Central Board of Directors in RBI board". 04-04-2013.

^ "Chakrabarty re-appointed RBI Deputy Governor". 13June 2012.

^ "About us, Organisation and Functions". RBI. Retrieved 2010-08-20.

^ "Reserve Bank of India". Rbi.org.in. Retrieved 2011-09-16.

^ "History of Reserve Bank". Retrieved 2009-02-24.

^[http://rbidocs.rbi.org.in/rdocs/Publications/PDFs/RBIB140520012.pdfReserve Bank of India, brochure, www.rbi.org.in]

^ "RBI launches website to explain detection of fake currency". Times of India. 8 July 2012.

^ Samarjit Das, Kaushik Bhattacharya: Price convergence across regions in India in Empirical Economics (2008) 34:299–313, S. 312.

^ Alpana Sivam, Sadasivam Karuppannan: Role of state and market in housing delivery for low-income groups in India in Journal of Housing and the Built Environment 17: 69–88, 2002, S.85.

^ "Indian banks can weather impact of drought: RBI". 07-08-2012.

External links[edit]

* * | Wikimedia Commons has media related to: Reserve Bank of India |

Reserve Bank of India Ombudsman site

[show]

[show]

[show]

-

Federal Reserve System

From Wikipedia, the free encyclopedia "FRB" and "FED" redirect here. For other uses, see FRB (disambiguation) and FED (disambiguation).

"FRB" and "FED" redirect here. For other uses, see FRB (disambiguation) and FED (disambiguation).Federal Reserve System

Seal of the Federal Reserve System Flag of the Federal Reserve System Headquarters Eccles Building, Washington, D.C. Established December 23, 1913 Chairman Ben Bernanke Central bank of United States Currency United States dollar ISO 4217 Code USD Base borrowing rate 0%–0.25%[1] Website www.FederalReserve.gov Part of a series on Government Public finance

Banking in

the United StatesMonetary policy Federal Reserve System Regulation Lending Deposit accounts Deposit account insurance Electronic funds transfer (EFT) Check clearing system Types of bank charter The Federal Reserve System (also known as the Federal Reserve, and informally as the Fed) is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, largely in response to a series of financial panics, particularly a severepanic in 1907.[2][3][4][5][6][7] Over time, the roles and responsibilities of the Federal Reserve System have expanded and its structure has evolved.[3][8]Events such as the Great Depression were major factors leading to changes in the system.[9]

The U.S. Congress established three key objectives for monetary policy in the Federal Reserve Act: Maximum employment, stable prices, and moderate long-term interest rates.[10] The first two objectives are sometimes referred to as the Federal Reserve's dual mandate.[11] Its duties have expanded over the years, and today, according to official Federal Reserve documentation, include conducting the nation's monetary policy, supervising and regulating banking institutions, maintaining the stability of the financial system and providing financial services to depository institutions, the U.S. government, and foreign official institutions.[12] The Fed also conducts research into the economy and releases numerous publications, such as the Beige Book.

The Federal Reserve System's structure is composed of the presidentially appointed Board of Governors (or Federal Reserve Board), the Federal Open Market Committee (FOMC), twelve regional Federal Reserve Banks located in major cities throughout the nation, numerous privately owned U.S. member banks and various advisory councils.[13][14][15] The FOMC is the committee responsible for setting monetary policy and consists of all seven members of the Board of Governors and the twelve regional bank presidents, though only five bank presidents vote at any given time (the president of the New York Fed and four others who rotate through one-year terms). The Federal Reserve System has both private and public components, and was designed to serve the interests of both the general public and private bankers. The result is a structure that is considered unique among central banks. It is also unusual in that an entity outside of the central bank, namely the United States Department of the Treasury, creates the currency used.[16] According to the Board of Governors, the Federal Reserve System "is considered an independent central bank because its monetary policy decisions do not have to be approved by the President or anyone else in the executive or legislative branches of government, it does not receive funding appropriated by the Congress, and the terms of the members of the Board of Governors span multiple presidential and congressional terms."[17]

The authority of the Federal Reserve System is derived from statutes enacted by the U.S. Congress and the System is subject to congressional oversight. The members of the Board of Governors, including its chairman and vice-chairman, are chosen by the Presidentand confirmed by the Senate. The government also exercises some control over the Federal Reserve by appointing and setting the salaries of the system's highest-level employees. Nationally chartered commercial banks are required to hold stock in the Federal Reserve Bank of their region; this entitles them to elect some of the members of the board of the regional Federal Reserve Bank. Thus the Federal Reserve system has both public and private aspects.[18][19][20][21] The U.S. Government receives all of the system's annual profits, after a statutory dividend of 6% on member banks' capital investment is paid, and an account surplus is maintained. In 2010, the Federal Reserve made a profit of $82 billion and transferred $79 billion to theU.S. Treasury.[22] This was followed at the end of 2011 with a transfer of $77 billion in profits to the U.S. Treasury Department.[23]

Contents

[hide]- 1 Purpose

- 2 Structure

- 3 Monetary policy

- 4 History

- 5 Measurement of economic variables

- 6 Budget

- 7 Net worth

- 8 Criticism

- 9 See also

- 10 References

- 11 Bibliography

- 12 External links

Purpose[edit]

The primary motivation for creating the Federal Reserve System was to address banking panics.[3] Other purposes are stated in the Federal Reserve Act, such as "to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes".[24] Before the founding of the Federal Reserve System, the United States underwent several financial crises. A particularly severe crisis in 1907 led Congress to enact the Federal Reserve Act in 1913. Today the Federal Reserve System has responsibilities in addition to ensuring the stability of the financial system.[25]

Current functions of the Federal Reserve System include:[12][25]

- To address the problem of banking panics

- To serve as the central bank for the United States

- To strike a balance between private interests of banks and the centralized responsibility of government

- To supervise and regulate banking institutions

- To protect the credit rights of consumers

- To manage the nation's money supply through monetary policy to achieve the sometimes-conflicting goals of

- To maintain the stability of the financial system and contain systemic risk in financial markets

- To provide financial services to depository institutions, the U.S. government, and foreign official institutions, including playing a major role in operating the nation's payments system

- To facilitate the exchange of payments among regions

- To respond to local liquidity needs

- To strengthen U.S. standing in the world economy

Addressing the problem of bank panics[edit]

Further information: bank run and fractional-reserve bankingBanking institutions in the United States are required to hold reserves – amounts of currency and deposits in other banks – equal to only a fraction of the amount of the banks' deposit liabilities owed to customers. This practice is called fractional-reserve banking. As a result, banks usually invest the majority of the funds received from depositors. On rare occasion, too many of the bank's customers will withdraw their savings and the bank will need help from another institution to continue operating; this is called a bank run. Bank runs can lead to a multitude of social and economic problems. The Federal Reserve System was designed as an attempt to prevent or minimize the occurrence of bank runs, and possibly act as a lender of last resort when a bank run does occur. Many economists, following Milton Friedman, believe that the Federal Reserve inappropriately refused to lend money to small banks during the bank runs of 1929.[27]

Elastic currency[edit]

One way to lessen the likelihood and the effect of bank runs is to have a money supply that can expand when money is needed. The use of the term "elastic currency" in the Federal Reserve Act does not imply only the ability to expand the money supply, but also the ability to contract the money supply. Some economic theories have been developed that support the idea of expanding or shrinking a money supply as economic conditions warrant. Elastic currency is defined by the Federal Reserve as:[28]

Currency that can, by the actions of the central monetary authority, expand or contract in amount warranted by economic conditions.Monetary policy of the Federal Reserve System is based partially on the theory that it is best overall to expand or contract the money supply as economic conditions change.

Check clearing system[edit]

Because some banks refused to clear checks from certain others during times of economic uncertainty, a check-clearing system was created in the Federal Reserve system. It is briefly described in The Federal Reserve System – Purposes and Functions as follows:[29]

By creating the Federal Reserve System, Congress intended to eliminate the severe financial crises that had periodically swept the nation, especially the sort of financial panic that occurred in 1907. During that episode, payments were disrupted throughout the country because many banks and clearinghouses refused to clear checks drawn on certain other banks, a practice that contributed to the failure of otherwise solvent banks. To address these problems, Congress gave the Federal Reserve System the authority to establish a nationwide check-clearing system. The System, then, was to provide not only an elastic currency – that is, a currency that would expand or shrink in amount as economic conditions warranted – but also an efficient and equitable check-collection system.Lender of last resort[edit]

In the United States, the Federal Reserve serves as the lender of last resort to those institutions that cannot obtain credit elsewhere and the collapse of which would have serious implications for the economy. It took over this role from the private sector "clearing houses" which operated during the Free Banking Era; whether public or private, the availability of liquidity was intended to prevent bank runs.

Emergencies[edit]

According to the Federal Reserve Bank of Minneapolis, "the Federal Reserve has the authority and financial resources to act as 'lender of last resort' by extending credit to depository institutions or to other entities in unusual circumstances involving a national or regional emergency, where failure to obtain credit would have a severe adverse impact on the economy."[30] The Federal Reserve System's role as lender of last resort has been criticized because it shifts the risk and responsibility away from lenders and borrowers and places it on others in the form of inflation.[31]

Fluctuations[edit]

Through its discount and credit operations, Reserve Banks provide liquidity to banks to meet short-term needs stemming from seasonal fluctuations in deposits or unexpected withdrawals. Longer term liquidity may also be provided in exceptional circumstances. The rate the Fed charges banks for these loans is the discount rate (officially the primary credit rate).

By making these loans, the Fed serves as a buffer against unexpected day-to-day fluctuations in reserve demand and supply. This contributes to the effective functioning of the banking system, alleviates pressure in the reserves market and reduces the extent of unexpected movements in the interest rates.[32] For example, on September 16, 2008, the Federal Reserve Board authorized an $85 billion loan to stave off the bankruptcy of international insurance giant American International Group (AIG).[33][34]

Central bank[edit]

Further information: Central bankIn its role as the central bank of the United States, the Fed serves as a banker's bank and as the government's bank. As the banker's bank, it helps to assure the safety and efficiency of the payments system. As the government's bank, or fiscal agent, the Fed processes a variety of financial transactions involving trillions of dollars. Just as an individual might keep an account at a bank, the U.S. Treasury keeps a checking account with the Federal Reserve, through which incoming federal tax deposits and outgoing government payments are handled. As part of this service relationship, the Fed sells and redeems U.S. government securities such as savings bonds and Treasury bills, notes and bonds. It also issues the nation's coin and paper currency. The U.S. Treasury, through its Bureau of the Mint andBureau of Engraving and Printing, actually produces the nation's cash supply and, in effect, sells the paper currency to the Federal Reserve Banks at manufacturing cost, and the coins at face value. The Federal Reserve Banks then distribute it to other financial institutions in various ways.[35] During the Fiscal Year 2008, the Bureau of Engraving and Printing delivered 7.7 billion notes at an average cost of 6.4 cents per note.[36]

Federal funds[edit]

Main article: Federal fundsFederal funds are the reserve balances (also called federal reserve accounts) that private banks keep at their local Federal Reserve Bank.[37][38] These balances are the namesake reserves of the Federal Reserve System. The purpose of keeping funds at a Federal Reserve Bank is to have a mechanism for private banks to lend funds to one another. This market for funds plays an important role in the Federal Reserve System as it is what inspired the name of the system and it is what is used as the basis for monetary policy. Monetary policy works partly by influencing how much interest the private banks charge each other for the lending of these funds.

Federal reserve accounts contain federal reserve credit, which can be converted into federal reserve notes. Private banks maintain theirbank reserves in federal reserve accounts.

Balance between private banks and responsibility of governments[edit]

The system was designed out of a compromise between the competing philosophies of privatization and government regulation. In 2006Donald L. Kohn, vice chairman of the Board of Governors, summarized the history of this compromise:[39]

Agrarian and progressive interests, led by William Jennings Bryan, favored a central bank under public, rather than banker, control. But the vast majority of the nation's bankers, concerned about government intervention in the banking business, opposed a central bank structure directed by political appointees. The legislation that Congress ultimately adopted in 1913 reflected a hard-fought battle to balance these two competing views and created the hybrid public-private, centralized-decentralized structure that we have today.In the current system, private banks are for-profit businesses but government regulation places restrictions on what they can do. The Federal Reserve System is a part of government that regulates the private banks. The balance between privatization and government involvement is also seen in the structure of the system. Private banks elect members of the board of directors at their regional Federal Reserve Bank while the members of the Board of Governors are selected by the President of the United States and confirmed by theSenate. The private banks give input to the government officials about their economic situation and these government officials use this input in Federal Reserve policy decisions. In the end, private banking businesses are able to run a profitable business while the U.S. government, through the Federal Reserve System, oversees and regulates the activities of the private banks.

Government regulation and supervision[edit]

The Federal Banking Agency Audit Act, enacted in 1978 as Public Law 95-320 and 31 U.S.C. section 714 establish that the Board of Governors of the Federal Reserve System and the Federal Reserve banks may be audited by the Government Accountability Office(GAO).[40] The GAO has authority to audit check-processing, currency storage and shipments, and some regulatory and bank examination functions, however there are restrictions to what the GAO may audit. Audits of the Reserve Board and Federal Reserve banks may not include:

- transactions for or with a foreign central bank or government, or nonprivate international financing organization;

- deliberations, decisions, or actions on monetary policy matters;

- transactions made under the direction of the Federal Open Market Committee; or

- a part of a discussion or communication among or between members of the Board of Governors and officers and employees of the Federal Reserve System related to items (1), (2), or (3).[41][42]

The financial crisis which began in 2007, corporate bailouts, and concerns over the Fed's secrecy have brought renewed concern regarding ability of the Fed to effectively manage the national monetary system.[43] A July 2009 Gallup Poll found only 30% of Americans thought the Fed was doing a good or excellent job, a rating even lower than that for the Internal Revenue Service, which drew praise from 40%.[44] The Federal Reserve Transparency Act was introduced by congressman Ron Paul in order to obtain a more detailed audit of the Fed. The Fed has since hired Linda Robertson who headed the Washington lobbying office of Enron Corp. and was adviser to all three of the Clinton administration's Treasury secretaries.[45][46][47][48]

The Board of Governors in the Federal Reserve System has a number of supervisory and regulatory responsibilities in the U.S. banking system, but not complete responsibility. A general description of the types of regulation and supervision involved in the U.S. banking system is given by the Federal Reserve:[49]

The Board also plays a major role in the supervision and regulation of the U.S. banking system. It has supervisory responsibilities for state-chartered banks[50] that are members of the Federal Reserve System, bank holding companies(companies that control banks), the foreign activities of member banks, the U.S. activities of foreign banks, and Edge Actand "agreement corporations" (limited-purpose institutions that engage in a foreign banking business). The Board and, under delegated authority, the Federal Reserve Banks, supervise approximately 900 state member banks and 5,000 bank holding companies. Other federal agencies also serve as the primary federal supervisors of commercial banks; the Office of the Comptroller of the Currency supervises national banks, and the Federal Deposit Insurance Corporation supervisesstate banks that are not members of the Federal Reserve System.Some regulations issued by the Board apply to the entire banking industry, whereas others apply only to member banks, that is, state banks that have chosen to join the Federal Reserve System and national banks, which by law must be members of the System. The Board also issues regulations to carry out major federal laws governing consumer credit protection, such as the Truth in Lending, Equal Credit Opportunity, and Home Mortgage Disclosure Acts. Many of these consumer protection regulations apply to various lenders outside the banking industry as well as to banks.

Members of the Board of Governors are in continual contact with other policy makers in government. They frequently testify before congressional committees on the economy, monetary policy, banking supervision and regulation, consumer credit protection, financial markets, and other matters.

The Board has regular contact with members of the President's Council of Economic Advisers and other key economic officials. The Chairman also meets from time to time with the President of the United States and has regular meetings with the Secretary of the Treasury. The Chairman has formal responsibilities in the international arena as well.Regulatory and oversight responsibilities[edit]

The board of directors of each Federal Reserve Bank District also has regulatory and supervisory responsibilities. If the board of directors of a district bank has judged that a member bank is performing or behaving poorly, it will report this to the Board of Governors. This policy is described in United States Code:[51]

Each Federal reserve bank shall keep itself informed of the general character and amount of the loans and investments of its member banks with a view to ascertaining whether undue use is being made of bank credit for the speculative carrying of or trading in securities, real estate, or commodities, or for any other purpose inconsistent with the maintenance of sound credit conditions; and, in determining whether to grant or refuse advances, rediscounts, or other credit accommodations, the Federal reserve bank shall give consideration to such information. The chairman of the Federal reserve bank shall report to the Board of Governors of the Federal Reserve System any such undue use of bank credit by any member bank, together with his recommendation. Whenever, in the judgment of the Board of Governors of the Federal Reserve System, any member bank is making such undue use of bank credit, the Board may, in its discretion, after reasonable notice and an opportunity for a hearing, suspend such bank from the use of the credit facilities of the Federal Reserve System and may terminate such suspension or may renew it from time to time.National payments system[edit]

The Federal Reserve plays an important role in the U.S. payments system. The twelve Federal Reserve Banks provide banking services to depository institutions and to the federal government. For depository institutions, they maintain accounts and provide various payment services, including collecting checks, electronically transferring funds, and distributing and receiving currency and coin. For the federal government, the Reserve Banks act as fiscal agents, paying Treasury checks; processing electronic payments; and issuing, transferring, and redeeming U.S. government securities.[52]

In passing the Depository Institutions Deregulation and Monetary Control Act of 1980, Congress reaffirmed its intention that the Federal Reserve should promote an efficient nationwide payments system. The act subjects all depository institutions, not just member commercial banks, to reserve requirements and grants them equal access to Reserve Bank payment services. It also encourages competition between the Reserve Banks and private-sector providers of payment services by requiring the Reserve Banks to charge fees for certain payments services listed in the act and to recover the costs of providing these services over the long run.

The Federal Reserve plays a vital role in both the nation's retail and wholesale payments systems, providing a variety of financial services to depository institutions. Retail payments are generally for relatively small-dollar amounts and often involve a depository institution's retail clients – individuals and smaller businesses. The Reserve Banks' retail services include distributing currency and coin, collecting checks, and electronically transferring funds through the automated clearinghouse system. By contrast, wholesale payments are generally for large-dollar amounts and often involve a depository institution's large corporate customers or counterparties, including other financial institutions. The Reserve Banks' wholesale services include electronically transferring funds through the Fedwire Funds Service and transferring securities issued by the U.S. government, its agencies, and certain other entities through the Fedwire Securities Service. Because of the large amounts of funds that move through the Reserve Banks every day, the System has policies and procedures to limit the risk to the Reserve Banks from a depository institution's failure to make or settle its payments.

The Federal Reserve Banks began a multi-year restructuring of their check operations in 2003 as part of a long-term strategy to respond to the declining use of checks by consumers and businesses and the greater use of electronics in check processing. The Reserve Banks will have reduced the number of full-service check processing locations from 45 in 2003 to 4 by early 2011.[53]

Structure[edit]

Main article: Structure of the Federal Reserve SystemThe Federal Reserve System has a "unique structure that is both public and private"[54] and is described as "independent within the government" rather than "independent of government".[55] The System does not require public funding, and derives its authority and purpose from the Federal Reserve Act, which was passed by Congress in 1913 and is subject to Congressional modification or repeal.[56] The four main components of the Federal Reserve System are (1) the Board of Governors, (2) the Federal Open Market Committee, (3) the twelve regional Federal Reserve Banks, and (4) the member banks throughout the country.

Board of Governors[edit]

Main article: Federal Reserve Board of GovernorsThe seven-member Board of Governors is a federal agency. It is charged with the overseeing of the 12 District Reserve Banks and setting national monetary policy. It also supervises and regulates the U.S. banking system in general.[57] Governors are appointed by the President of the United States and confirmed by the Senate for staggered 14-year terms.[32] One term begins every two years, on February 1 of even-numbered years, and members serving a full term cannot be renominated for a second term.[58] "[U]pon the expiration of their terms of office, members of the Board shall continue to serve until their successors are appointed and have qualified." The law provides for the removal of a member of the Board by the President "for cause".[59] The Board is required to make an annual report of operations to the Speaker of the U.S. House of Representatives.

The Chairman and Vice Chairman of the Board of Governors are appointed by the President from among the sitting Governors. They both serve a four-year term and they can be renominated as many times as the President chooses, until their terms on the Board of Governors expire.[60]

List of members of the Board of Governors[edit]

The current members of the Board of Governors are as follows:[58]

Commissioner Entered office[61] Term expires Ben Bernanke

(Chairman)February 1, 2006 January 31, 2020

January 31, 2014 (as Chairman)Janet Yellen

(Vice Chairman)October 4, 2010 January 31, 2024

October 4, 2014 (as Vice Chairman)Elizabeth A. Duke August 5, 2008 January 31, 2012 Daniel Tarullo January 28, 2009 January 31, 2022 Sarah Bloom Raskin October 4, 2010 January 31, 2016 Jerome H. Powell May 25, 2012 January 31, 2014 Jeremy C. Stein May 30, 2012 January 31, 2018 Nominations and confirmations[edit]

In late December 2011, President Barack Obama nominated Stein, a Harvard University finance professor and a Democrat, and Powell, formerly of Dillon Read, Bankers Trust[62] and The Carlyle Group[63] and a Republican. Both candidates also have Treasury Departmentexperience in the Obama and George H.W. Bush administrations respectively.[62]

"Obama administration officials [had] regrouped to identify Fed candidates after Peter Diamond, a Nobel Prize-winning economist, withdrew his nomination to the board in June [2011] in the face of Republican opposition. Richard Clarida, a potential nominee who was a Treasury official under George W. Bush, pulled out of consideration in August [2011]", one account of the December nominations noted.[64] The two other Obama nominees in 2011, Yellen and Raskin,[65] were confirmed in September.[66] One of the vacancies was created in 2011 with the resignation of Kevin Warsh, who took office in 2006 to fill the unexpired term ending January 31, 2018, and resigned his position effective March 31, 2011.[67][68] In March 2012, U.S. Senator David Vitter (R, LA) said he would oppose Obama's Stein and Powell nominations, dampening near-term hopes for approval.[69] However Senate leaders reached a deal, paving the way for affirmative votes on the two nominees in May 2012 and bringing the board to full strength for the first time since 2006[70] with Duke's service after term end.

Federal Open Market Committee[edit]

Main article: Federal Open Market CommitteeThe Federal Open Market Committee (FOMC) consists of 12 members, seven from the Board of Governors and 5 of the regional Federal Reserve Bank presidents. The FOMC oversees open market operations, the principal tool of national monetary policy. These operations affect the amount of Federal Reserve balances available to depository institutions, thereby influencing overall monetary and credit conditions. The FOMC also directs operations undertaken by the Federal Reserve in foreign exchange markets. The president of the Federal Reserve Bank of New York is a permanent member of the FOMC; the presidents of the other banks rotate membership at two- and three-year intervals. All Regional Reserve Bank presidents contribute to the committee's assessment of the economy and of policy options, but only the five presidents who are then members of the FOMC vote on policy decisions. The FOMC determines its own internal organization and, by tradition, elects the Chairman of the Board of Governors as its chairman and the president of the Federal Reserve Bank of New York as its vice chairman. It is informal policy within the FOMC for the Board of Governors and the New York Federal Reserve Bank president to vote with the Chairman of the FOMC; anyone who is not an expert on monetary policy traditionally votes with the chairman as well; and in any vote no more than two FOMC members can dissent.[71] Formal meetings typically are held eight times each year in Washington, D.C. Nonvoting Reserve Bank presidents also participate in Committee deliberations and discussion. The FOMC generally meets eight times a year in telephone consultations and other meetings are held when needed.[72]

Federal Advisory Council[edit]

Main article: Federal Advisory CouncilFederal Reserve Banks[edit]

Main article: Federal Reserve BankThere are 12 Federal Reserve Banks located in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago,St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each reserve Bank is responsible for member banks located in its district. The size of each district was set based upon the population distribution of the United States when the Federal Reserve Act was passed. Each regional Bank has a president, who is the chief executive officer of their Bank. Each regional Reserve Bank's president is nominated by their Bank's board of directors, but the nomination is contingent upon approval by the Board of Governors. Presidents serve five-year terms and may be reappointed.[73]

Each regional Bank's board consists of nine members. Members are broken down into three classes: A, B, and C. There are three board members in each class. Class A members are chosen by the regional Bank's shareholders, and are intended to represent member banks' interests. Member banks are divided into three categories large, medium, and small. Each category elects one of the three class A board members. Class B board members are also nominated by the region's member banks, but class B board members are supposed to represent the interests of the public. Lastly, class C board members are nominated by the Board of Governors, and are also intended to represent the interests of the public.[74]